Advocates made strides in protecting consumers from predatory auto sales, lending, junk fees, and medical debt and from abusive practices in credit reporting, tenant screening, debt collection, utilities, student loans, and other areas that harm low-income consumers, strip wealth from communities – especially communities of color – and deplete wealth that families need for generational financial stability.

Access to Justice/Arbitration

Working with a coalition to end fine print traps, NCLC joined over 100 other groups in petitioning the Consumer Financial Protection Bureau (CFPB) to create a rule to restore the right of all Americans to file a case in court rather than be forced into arbitration by big banks and financial services corporations. In addition to the letter, signed by more than 100 consumer protection, civil rights, and labor organizations, the coalition submitted petitions signed by more than 17,000 people, showing grassroots support for ending forced arbitration.

Advocates spoke out in favor of the Forced Arbitration Injustice Repeal (FAIR) Act, federal legislation that would ensure that workers, consumers, servicemembers, nursing home residents, ordinary investors, and small businesses harmed by bad actors will be able to bring valid claims in court, and would not be forced into private, secretive, corporate-controlled arbitration systems that nonnegotiable contracts overwhelmingly require. The FAIR Act would apply to cases involving consumer, civil rights, employment, or antitrust violations, and would ensure that harmed individuals in these cases can enforce related federal and state protections.

Advocates joined a letter urging that proposed SELF DRIVE Act legislation concerning autonomous vehicles prohibit forced arbitration clauses. “This moment presents an opportunity to ensure that a practice designed to deprive consumers of their constitutional rights not be allowed to continue into the next generation of vehicles,” advocates wrote.

Auto Finance & Sales

After urging the Federal Trade Commission (FTC) to issue a rule to protect consumers in car sales and finance transactions and providing substantive and detailed comments to the FTC’s proposed rule, advocates praised the FTC for issuing the Combating Auto Retail Scams (CARS) rule in mid-December. It requires dealers to provide an offering price in advertisements or discussions about a specific car, prohibits a number of misrepresentations that will allow the FTC to obtain consumer redress in its enforcement actions, and prohibits dealers from charging for add-ons without express consent.

NCLC is now arming itself to defend the rule from inevitable industry challenges in Congress and the courts as well as to push the FTC to build on the rule with additional important and straightforward consumer protections such as creating a 30-day cooling-off period within which consumers could get a full refund for add-ons they were pressured to buy, and requiring credit contracts to state that the signed contract and its credit or lease terms are final and binding, notwithstanding any other agreements between the parties or any other notice provided by the dealer, which would stop yo-yo sales.

NCLC, along with the Consumer Federation of America, Consumer Reports, and Empire Justice Center, filed an amicus brief in the U.S. District Court for the Southern District of New York in support of the CFPB and the New York Attorney General’s opposition to a motion to dismiss its case against Credit Acceptance Corporation (CAC). The brief supports the suit, which alleges that CAC profits from transactions that are unnecessarily expensive and designed to fail, creating a perverse incentive to put consumers into harmful transactions. NCLC hopes the action encourages healthy access to credit to allow people to purchase cars they need but ensures both the consumer and the finance provider are motivated to see the consumer come out of the transaction having successfully paid for the car.

Banking, Payments, & Remittances

NCLC worked on multiple fronts to stop fraudsters from stealing from consumers through payment fraud, including an op-ed urging stronger fraud protections in person-to-person payment systems and multiple other statements in the media; meetings with regulators; assistance to attorneys handling fraud cases; comments urging the FTC and other regulators to increase collaboration to address fraud; a letter urging the FTC and CFPB to address the use of deep fakes; comments urging NACHA to improve protections against fraudulently induced electronic payments; and support for a California bill to ensure that elderly victims of financial scams can hold negligent banks accountable for assisting in the financial exploitation of older Californians.

NCLC sent a letter to the CFPB requesting a review of current regulations to improve usefulness and transparency of remittance disclosures and followed up with a group letter on recommendations to make international remittance pricing more transparent.

NCLC applauded guidance from the White House and the FTC prohibiting bank fees for consumers to obtain basic information about their own accounts.

NCLC opposed a crypto-asset bill and submitted a statement for a congressional hearing highlighting the risks of crypto-assets.

NCLC provided comments regarding false advertising, misrepresentation of insured status, and misuse of the FDIC’s name or logo.

NCLC joined an amicus brief with Public Counsel to assert that money transfer businesses are financial institutions covered by the Right to Financial Privacy Act (RFPA), and therefore must protect the financial records of remittance senders who are predominantly immigrants and who rely on money transfer businesses for their transactions.

NCLC sent a letter to the CFPB requesting a review of current regulations to improve usefulness and transparency of remittance disclosures and followed up with a group letter on recommendations to make international remittance pricing more transparent.

NCLC applauded guidance from the White House and the FTC prohibiting bank fees for consumers to obtain basic information about their own accounts.

NCLC opposed a crypto-asset bill and submitted a statement for a congressional hearing highlighting the risks of crypto-assets.

NCLC provided comments regarding false advertising, misrepresentation of insured status, and misuse of the FDIC’s name or logo.

NCLC joined an amicus brief with Public Counsel to assert that money transfer businesses are financial institutions covered by the Right to Financial Privacy Act (RFPA), and therefore must protect the financial records of remittance senders who are predominantly immigrants and who rely on money transfer businesses for their transactions.

In August, NCLC joined other groups to send a letter to the FTC illustrating the importance of information sharing and collaboration between state and federal law enforcement agencies charged with protecting the public from fraud and other unfair, deceptive, and abusive business practices.

Consumer Financial Protection Bureau

NCLC weighed in on the U.S. Supreme Court’s announcement that it would review Consumer Financial Services Association of America v. Consumer Financial Protection Bureau, a dangerous decision by the U.S. Court of Appeals for the Fifth Circuit that held that the funding mechanism established by Congress when it created the CFPB was unconstitutional. NCLC joined nine other consumer advocacy organizations in submitting an amicus brief urging SCOTUS to uphold the constitutionality of the CFPB.

More than 80 consumer and advocacy organizations sent a letter to Congress in support of the CFPB as it prepared for its semi-annual review. NCLC joined comments in support of the CFPB’s Statement of Policy regarding abusive practices that impact wide swaths of American consumers and have an especially negative impact on vulnerable and marginalized communities.

NCLC urged our supporters and allies to take action by writing letters to their members of Congress and submitting letters to the editor of local newspapers in support of the CFPB.

Credit Reporting & Data Fairness

In an exciting development, the CFPB has launched a rulemaking under the Fair Credit Reporting Act (FCRA) to reform the credit reporting system and promote data fairness for consumers. The CFPB issued a Request for Information (RFI) on data brokers in March 2023, to which NCLC filed comprehensive and detailed comments. In September 2023, the CFPB released an outline of proposals for the FCRA rulemaking as part of its small business review process. The proposals focused on three areas: (1) regulating data brokers under the FCRA; (2) eliminating medical debt on credit reports; and (3) reforms to the credit reporting dispute process.

NCLC led advocates in praising the CFPB when it issued these proposals, and once again filed comprehensive and detailed comments in response. The proposals, if adopted, will provide major benefits for consumers and are the culmination of decades of advocacy by NCLC regarding credit reporting and other types of consumer reporting.

Tenant screening reports, which are regulated under the FCRA, have become the focus of attention by regulators given the rental housing crisis in this country. The CFPB and FTC issued a request for information on tenant screening. In response, NCLC supplied extensive comments and then turned them into a major report, “Digital Denials: How Abuse, Bias, and Lack of Transparency in Tenant Screening Harm Renters.” NCLC’s report explores how tenant screening reports harm renters and have a disparate impact on Black and Latino/Hispanic renters. The report analyzes the results of a survey of attorneys, advocates and counselors that NCLC conducted, discusses the most significant problems with tenant screening in depth, and makes recommendations to CFPB, FTC, Congress, and state legislatures.

NCLC has urged the CFPB to tackle other critical issues in its FCRA rulemaking. In a March 2023 petition, advocates urged the CFPB to (1) adopt strict requirements to regulate the furnishing of negative information by debt collectors, which is often the source of errors and abuses in credit reports; (2) require the credit bureaus to provide translation of credit reports into the eight languages most frequently used by limited English proficient consumers; and (3) establish an Office of Ombudsperson to assist consumers who have been unable to fix errors in their credit reports or other consumer reports.

Advocates expressed strong opposition to H.R. 1165, the Data Privacy Act of 2023, a bill consumer groups believe would actually deprive consumers of important protections under state law, and offer little or no real new protections at the federal level. While claiming to strengthen the Gramm-Leach-Bliley Act (GLBA) and increase consumer protections, H.R. 1165 actually would result in fewer rights for consumers, because it would deprive them of important – and enforceable – rights under state law, by preempting the laws in over half states that govern credit reporting and in some cases, other types of consumer reporting.

Criminal Justice

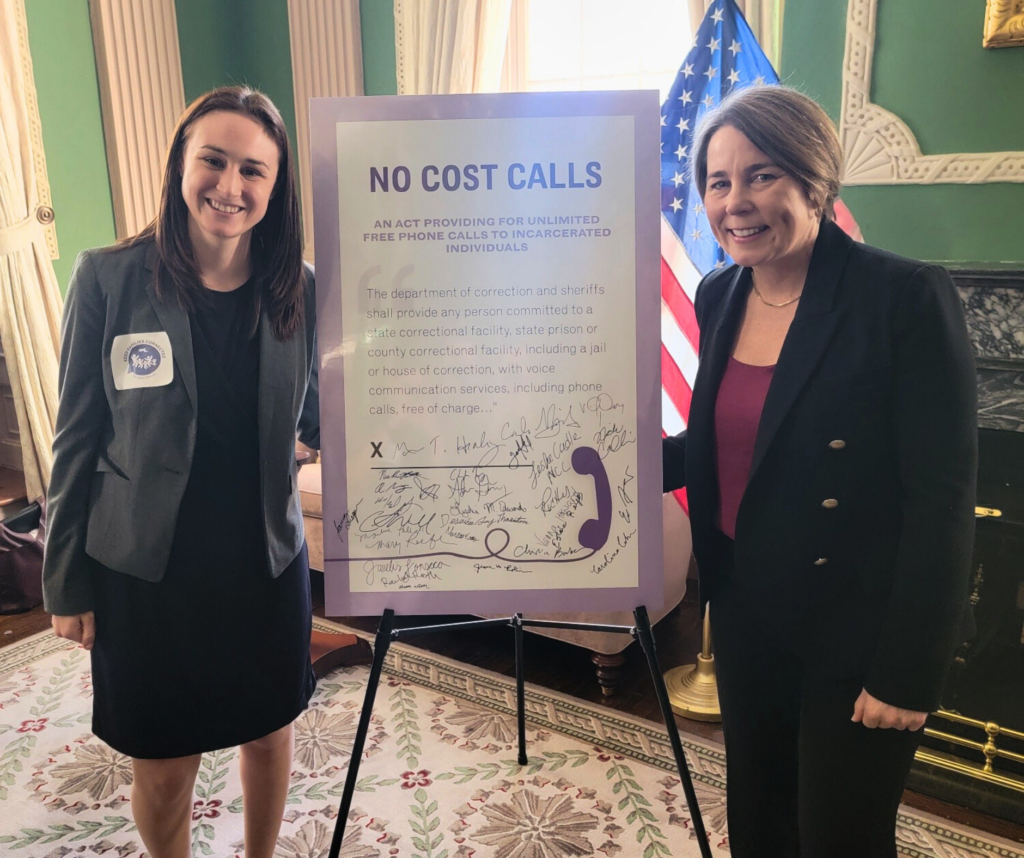

NCLC, along with a coalition that includes directly impacted people, testified and ultimately persuaded the Massachusetts legislature and governor to make phone calls free for people incarcerated in the state’s prisons and jails and their families. Effective December 1, Massachusetts became the fifth state to make prison phone calls free and the first to include free phone calls from county jails.

On the federal level, NCLC advocates contributed to the passage of the Martha Wright-Reed Just and Reasonable Communications Act, which directs the FCC to ensure that companies providing communication services to people who are incarcerated are no longer able to charge outrageously high rates and fees for these services. We had long advocated for this legislation as part of a well-established, bipartisan coalition and continue to provide our expertise as the FCC implements the law.

NCLC advocates identified the President’s administration-wide effort to address junk fees as a unique opportunity to draw attention to private profiteering in the correctional context and to the fees imposed on incarcerated people and their loved ones. When the Federal Trade Commission (FTC) issued an Advanced Notice of Proposed Rulemaking on junk fees, we provided comments, joined by over two dozen other advocacy groups, drawing attention to these harmful fees and leading the FTC to specifically acknowledge them in its subsequent Notice of Proposed Rulemaking.

NCLC advocates submitted extensive comments to the Bureau of Prisons opposing a proposed rule that would allow seizure of portions of incarcerated people’s wages and the bulk of the funds that family members send to them, and apply the seized funds to fines, fees, and restitution.Seizure of wages would severely limit the ability of incarcerated people to afford medical co-pays, over-the-counter medications and hygiene products, and communications with attorneys and loved ones. As a result of the negative comments it generated, the BOP has unofficially put the proposed rule on pause, but NCLC continues to work in coalition to ensure it is formally withdrawn.

NCLC’s litigation team helped win an initial victory as co-counsel in In re California Bail Bond Antitrust Litig., No. 19-CV-00717-JST (N.D. Cal.), a case alleging that an antitrust conspiracy has fixed the prices of the premiums paid for commercial bail bonds since at least 2004. We defeated multiple motions to dismiss certain defendants and claims, and the case has proceeded to discovery.

Debt & Bankruptcy

Medical debt continues to be a leading reason consumers are contacted by debt collectors. NCLC works to analyze and reduce the burden of medical debt, eliminate abusive debt collection, stop credit reporting of medical debt, and prevent medical debt at the outset.

In the states, NCLC provided testimony in support of a Colorado bill that would prohibit the reporting of medical debts by credit bureaus as well as providing technical assistance on a similar New York State bill and testimony in support of a Medical Debt Protection Act in Delaware. All three bills passed, and Colorado and New York became the first states to ban medical debts on credit reports.

A Digital Library article, Widespread FDCPA Violations in Collection of Medical Debt, sets out common situations where medical debt is not owed or is owed in a lesser amount than the amount sought and then describes how an FDCPA claim can successfully challenge such medical debt collection.

On the topic of nursing home debt collection, NCLC submitted testimony in response to a request for feedback on the state of nursing home debt collection in New York and produced an issue brief addressing frequently asked questions, including whether a nursing home can force a resident’s family and friends to pay the bill.

NCLC cosponsored a bill in California that removes the last vestiges of debtors’ prisons in the state. Signed into law in October, the law ensures that no one in the state can be imprisoned because they owe a consumer debt. The measure, Assembly Bill 1119, was authored by Assemblymember Buffy Wicks and its other cosponsor was the California Low Income Consumer Coalition.

In its annual No Fresh Start Report, NCLC examined exemption laws in every state, rating how well they protect consumers and their families from poverty. The 2023 report revealed that few states’ exemption laws meet even the most basic standards in protecting wages, cars, the family home, bank accounts, and household goods. The report takes into account victories in the states, including an earmarked $500 self-executing bank account protection in Maryland and a significant overhaul of the exemption statute in New Mexico resulting in $190 a week more in wages being protected from seizure and greater protection of the home and the family car.

NCLC continued to work to increase access to bankruptcy for low-income consumers and expand the relief available. NCLC and the National Association of Consumer Advocates (NACA) joined an amicus brief prepared by Public Citizen in the Supreme Court case of Lac Du Flambeau v. Coughlin. In June, the Court held that the Bankruptcy Code unequivocally abrogates the sovereign immunity of all governments, including federally recognized Indian tribes.

A Digital Library article examined the decision of the Supreme Court in Bartenwerfer v. Buckley and the critical distinctions between the business and personal partnerships, including implications for divorced or separated debtors and victims of economic abuse and coerced debt. The article also discusses five potential ways for these consumer debtors to distinguish the Court’s holding and preserve their right to discharge debts that were fraudulently obtained by a co-obligor.

Energy, Utilities, & Telecommunications

After NCLC proposed a five-tiered discount rate for utility customers in Illinois to make gas rates more affordable for low-income residents, the Illinois Commerce Commission adopted the proposed discount rate, as well as adopting NCLC and coalition recommendations to reduce flat-rate customer charges. The ruling will be a model for utility commissions across the country to create protections for low-income utility customers. In another proceeding, the Commission adopted a new rate structure aimed at reducing involuntary electricity shut-offs.

With the United Church of Christ Media Justice Ministry, NCLC produced a State Digital Justice Advocacy Toolkit that contains resources to help frontline groups that are working to provide broadband and communication assistance to incarcerated people, people with disabilities, low-income households, veterans, aging and rural populations, people facing language barriers, members of racial or ethnic minorities, and other underserved groups.

NCLC advocates continue to work to persuade Congress to extend the Affordable Connectivity Program. More than 21 million households have enrolled in the program – including millions of households with school-aged children. But that represents less than half of the nearly 50 million income-eligible households, and funding for the ACP is projected to run out before the end of the 2023-2024 school year.

NCLC advocacy supported better Home Appliance Efficiency Standards, stronger drinking water rules to ensure affordable drinking water, continued funding of the Low Income Household Water Assistance Program (LIHWAP) program to help families with growing water debt and rising water costs, and improved standards for refrigerators and freezers and refrigerators and clothes washers.

NCLC and the National Housing Law Project submitted comments in strong support of the CFPB’s proposed consumer protection regulations for Property Assessed Clean Energy (PACE) loans, with recommendations to strengthen the proposal’s protection against the consumer abuses that have plagued this program. Residential PACE programs authorize loans typically offered by contractors going door-to-door for home improvements that claim to improve energy efficiency. Unlike standard mortgage loans, PACE loans are property tax liens collected through a tax assessment that do not comply with mortgage protections and take priority over any existing mortgage.

In Massachusetts, NCLC provided written testimony in support of legislation to end the sales of competitive retail electric supply to individual households and will continue to urge the legislature to enact it in 2024. Advocates also provided testimony in support of S. 2106 and H. 3196, An Act Relative to Electric Ratepayer Protections, legislation to end the sales of competitive retail electric supply to individual households. In addition, with a coalition including the Massachusetts Attorney General’s Office, NCLC produced a major report on how to incorporate community voices into the commonwealth’s energy regulatory process.

Along with advocacy partners from Public Citizen, Pennsylvania Utility Law Project, and Maryland Energy Advocates Coalition, NCLC filed comments to the FTC urging the agency to strengthen its rules about environmental claims made in marketing, to crack down on “greenwashing.”

The Inflation Reduction Act creates new programs to help pay for home energy efficiency upgrades for low-income and moderate-income consumers, but only if these programs contain adequate consumer protections. NCLC submitted comments to the Department of Energy and to the National Association of State Energy Offices (NASEO) detailing the consumer protections that will be needed to safely implement the Home Energy Rebate programs in the IRA.

NCLC’s input to US HHS and DOE helped shape agency guidance for necessary consumer protections in new low-income community solar programs under development.

NCLC submitted comments to the Treasury Department regarding programs to support affordable and accessible used EV purchase incentives and Treasury incorporated some of our recommendations in its guidance.

High-Cost Credit

NCLC’s work in the high-cost credit space focused heavily on “rent-a-bank” evasions of state interest rate caps and on other fintech evasions.

Advocates drafted a Digital Library article focused on lesser-known angles to challenge rent-a-bank schemes in court and led a coalition urging the FDIC to downgrade three banks engaged in predatory rent-a-bank lending. NCLC applauded a new Colorado law, that prevents out-of-state banks from helping predatory lenders evade the state rate caps. NCLC had testified in support of the new law when the state legislature was considering the bill. NCLC also praised actions taken by the District of Columbia, Colorado, and Iowa to crack down on high-interest loans laundered through banks.

NCLC submitted a letter joined by over 100 groups opposing a federal bill that would exempt fintech cash advances from the Truth in Lending Act; opposed a Nevada bill exempting the advances from state credit laws and urged the new Arizona Attorney General to repeal her predecessor’s earned wage advance guidance; led two sets of comments to the California Department of Financial Protection and Innovation on proposed rules on earned wage and other fintech cash advances, and praised California, Connecticut, and the District of Columbia for issuing orders against fintech payday lenders that solicit “tips.” NCLC published several issue briefs on fintech cash advances highlighting data on the 330% average APR; urging that workers should not pay to be paid; and providing state recommendations, jointly with the Center for Responsible Lending, for earned wage and fintech cash advances.

NCLC supported a federal bill to cap interest rates at 36%.

NCLC took the lead on consumer group comments in support of the CFPB proposal to limit credit card late fees to $8 and joined a coalition letter to President Biden and the CFPB supporting lover credit card late fees.

In November, NCLC released its annual report, Predatory Installment Lending in the States: How Well Do the States Protect Consumers Against High-Cost Installment Loans? (2023)

NCLC testified at a CFPB field hearing and submitted comments to the CFPB, HHS, and Treasury expressing our appreciation for their engagement in an extensive examination of medical payment products and their impact on vulnerable consumers. NCLC’s April 2023 report Health Care Plastic: The Risks of Medical Credit Cards discusses one type of medical payment product–medical credit cards–in depth, presents the results of a survey of legal services attorneys, private attorneys, and other advocates regarding their clients’ experiences with medical credit cards, and concludes with recommendations.

Homeownership & Foreclosure

NCLC continues to play an important role in crafting systems to assist homeowners facing foreclosure. NCLC, working with industry allies, successfully persuaded the CFPB to build on lessons learned from COVID and begin to rewrite the mortgage servicing rules that apply to the vast majority of mortgage loans. NCLC also petitioned the CFPB to expand the coverage of the regulation and to improve language access for borrowers with limited English proficiency.

For many years, NCLC advocates have called property tax lien sales The Other Foreclosure Crisis. In May, the U.S. Supreme Court held in Tyler v. Hennepin that when a local government takes a home at a property tax foreclosure and keeps the homeowner’s equity after the tax debt is paid, it violates the Takings Clause of the Fifth Amendment to the United States Constitution. NCLC had joined an amicus brief prepared by AARP in support of this position. Following the decision, NCLC educated attorneys and other advocates on the import of the decision and the need for states to bring their laws into alignment with it.

NCLC urged the Department of Veterans Affairs to stop unnecessary foreclosures on Veterans and active-duty service members in financial distress while a new program is being rolled out. In November, the VA announced a six-month foreclosure pause, which will allow time for implementation of the VA Servicing Purchase (VASP) program and prevent thousands of families from losing their homes unnecessarily. NCLC has called for VASP to include a fair system for providing borrower payment relief and for a public process in developing VASP. Back in January, NCLC submitted joint comments drawing the VA’s attention to this looming problem and urging it to expand home retention alternatives for borrowers with VA-guaranteed loans who were facing financial difficulties.

In response to comments led by NCLC, HUD refined its innovative Payment Supplement Partial Claim program, which aims to provide payment relief in a high interest rate environment to borrowers who face financial hardship. It is expected to become effective in 2024. NCLC led an effort to ensure the release of the new program with 63 organizations signing on to our letter. HUD also made significant improvements to its home preservation options for reverse mortgage borrowers at risk of foreclosure, following through on a number of NCLC’s recommendations in our Unmet Promise report. HUD released a new rule on FHA borrower engagement, which incorporated many of our recommendations in NCLC’s letter to HUD and NCLC led an effort to support the rule with 67 organizations signing on to a comment letter.

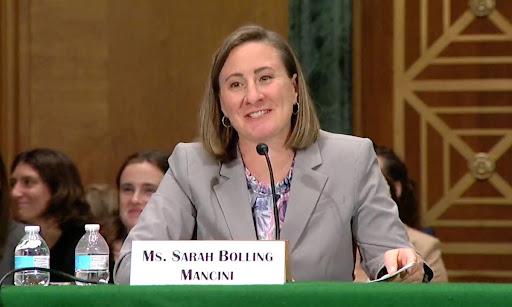

Testifying before the Senate Banking Subcommittee on Housing, Transportation, and Community Development, NCLC Co-Director of Advocacy Sarah Bolling Mancini reported that alternative home financing transactions such as land contracts and leases with option to buy do not provide a meaningful pathway to homeownership. Rather, land contracts and leases with option to buy are both costly and destructive detours that diminish the likelihood that consumers entering into these contracts will ever own a home. NCLC has long focused on these dangerous transactions.

NCLC issued a report examining the unique issues heirs face when inheriting a home with an overdue property tax bill and the disproportionate impact on Black and Latino wealth building. Some heirs may not even know they owe taxes on the property – leading to tax liens and even foreclosure. The report discusses the problems of “heirs property” or “tangled title” and recommends steps states can take to prevent property tax foreclosures and preserve homeownership.

In response to NCLC’s January 2023 report detailing serious issues with the bulk sales of federally backed loans to private equity companies and NCLC’s work with the Senate, the Federal Housing Finance Agency (FHFA) issued guidance in a June 2023 fact sheet that significantly improved the bulk sale process. The fact sheet announced improved data practices and indicated that loans in forbearance will not be sold and more homeowners will be eligible for payment deferrals.

Advocates welcomed a long-sought decision by Fannie Mae and Freddie Mac that requires lenders selling loans to them to collect information onborrowers’ preferred language, as well as any housing counseling services they’ve used. Fannie and Freddie now alsorequire mortgage servicers to obtain and maintain this information, along with other fair lending data, and transfer this information whenever servicing of the loan is transferred throughout the mortgage term. Both requirements empower lenders and servicers to better serve borrowers with limited English proficiency and improve the availability of fair lending data across the industry. FHFA is now proposing to codify this requirement in regulation, along with several enhancements to its Fair Lending Oversight program and the Equitable Housing Finance Plan framework. NCLC took a lead role in preparing groupcomments in support of this proposed rule. FHA also began requiring lenders to collect information on borrower language preference in August and published a series of translated mortgage documents in the top five most commonly spoken languages among U.S. individuals with Limited English Proficiency.

NCLC took the lead on preparing and submitting group comments to the White House Task Force on New Americans, calling on the Biden Administration to focus its attention on language access within our consumer financial markets, particularly in mortgage servicing and debt collection. NCLC also joined comments submitted on behalf of civil rights and consumer advocacy organizations in support of the Federal Housing Finance Agency’s notice of proposed rulemaking on Equitable Housing Finance and Fair Lending Supervision, urging FHFA to incorporate greater accountability and transparency into its Equitable Housing Finance Plan Framework and to improve language access in mortgage loan origination and servicing.

Advocates commended the FHFA for taking what advocates referred to as a critical first step in the journey to create a more equitable system for creditworthy borrowers. The updates help address persistent gaps in wealth and homeownership while also improving safety and soundness for Fannie Mae and Freddie Mac.

In the area of Manufactured Housing, NCLC advocates helped advocates in several states pass bills that give residents of manufactured home communities the opportunity to purchase the land on which their homes sit. Maine and Connecticut in particular now have strong laws. Resident ownership transforms manufactured home communities, ensuring that they remain stable, vibrant, well-maintained, and affordable.

In comments to the USDA Rural Housing Service (RHS), NCLC supported RHS’s use of Mortgage Recovery Advances to help borrowers reinstate past due mortgage amounts and defer principal to the end of the borrowers’ loan term at 0% interest.

NCLC submitted comments urging HUD to finalize and promulgate proposed regulations that would establish the necessary framework for a successful default servicing program and supplement guidance established by the Real Estate Settlement Procedures Act (RESPA). We made a number of suggestions to improve the proposed regulations as a way of avoiding unnecessary foreclosures for Native American borrowers.

Junk Fees

NCLC continues to work to bring an end to junk fees on bank accounts, credit cards, rental agreements, and other goods and services and junk fees tacked onto debts by debt collectors and by jails and prisons for necessities.

NCLC and 28 other organizations urged the Biden administration and the FTC to include justice-involved people in a broader effort to crack down on junk fees and led consumer groups in submitting comprehensive comments regarding junk fees imposed by providers of consumer financial products and services.

NCLC released its report, Too Damn High: How Junk Fees Add to Skyrocketing Rents, and urged the FTC and CFPB to address the many fees charged to renters and rental housing applicants.

In October, in response to the comments it had received, the FTC proposed a rule that would restrict junk fees and require disclosure of hidden junk fees, including those imposed on renters, extensively referenced NCLC’s report that identified the many, unavoidable junk fees that tenants face.

Racial Justice

Following the U.S. Supreme Court’s radical decision in Students for Fair Admissions v. Harvard, NCLC called on the consumer law community to join NCLC in work to dismantle systemic racism and promote economic justice for all people. The decision disregards decades of federal precedent upholding the consideration of race in higher education admissions and ignores the legacy of discrimination in American society, and the daily lived experience of people of color. NCLC, as a partner in the struggle for equity and racial justice, will continue to fight for policies that dismantle systemic racism, lessen the racial wealth gap and expand educational opportunities for all Americans.

NCLC advocates applauded President Biden’s executive order on artificial intelligence as a much-needed first step in developing safeguards to ensure that this technology does not widen existing racial disparities in housing, lending, credit, and other consumer products that rely on algorithms and private consumer data, adding that it must be followed by meaningful legislative and regulatory action to build an effective structure to ensure that AI’s potential for progress outweighs its potential for damage.

NCLC prioritizes litigation that will advance racial justice and is currently counsel in Fair Housing Act cases in Michigan and Massachusetts. In July, Judge Angel Kelley (D. Mass) denied the Defendants’ motions to dismiss a case NCLC brought with Cohen Milstein Sellers & Toll and Greater Boston Legal Services. Louis, et al v. SafeRent Solutions.

In Louis, NCLC is challenging SafeRent’s tenant-screening algorithm, which calculates a “SafeRent Score” for property management companies to use to select tenants. The lawsuit alleges that the defendant’s use of the algorithm, which relies on past credit history and fails to consider housing vouchers, caused a disparate impact on low-income, Black and Hispanic prospective tenants under the FHA and violates Massachusetts’ anti-discrimination and consumer protection laws. Among other things, the Court found that our allegations that use of the “SafeRent Score” resulted in discrimination in the privilege of renting were sufficient to confer standing. The Court rejected SafeRent’s argument that the FHA does not apply to it as a tenant-screening service, finding that provision of the SafeRent Score is directly related to the rental transaction.

Robocalls & Texts

NCLC’s work this year to stop unwanted and illegal robocalls and text included bringing allied organizations together to file comprehensive comments and follow-up comments urging the FCC to do more to block unlawful text messages and focus on consent requirements. A July Digital Library article looked at strict new limits on the number of prerecorded collection calls that a debt collector can send to a consumer’s landline.

NCLC and other national groups recommended that the FCC require an automated opt-out mechanism for all prerecorded calls and provided recommendations for specific requirements for revocation of consent or requests that TCPA covered calls are stopped.

NCLC updated our Consumer Resources for Scam Calls and Texts document and led advocates in urging the FCC to adopt a set of best practices for legal callers that—if widely used—will likely eliminate many of the illegal calls plaguing subscribers’ telephone lines.

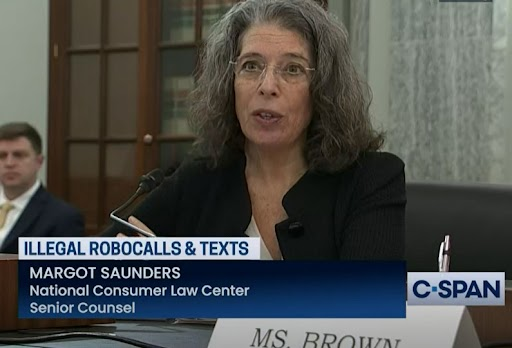

Margot Saunders, senior attorney, testified before the Senate Committee on Commerce, Science & Transportation Subcommittee on Communications, Media, and Broadband at a hearing titled, “Protecting Americans from Robocalls,” reporting that the current regulatory structure allows criminals access to Americans’ wallets: billions of dollars are stolen every year through scams executed over this nation’s telephone lines. At the same time, the combination of the scam calls along with the onslaught of unwanted—and mostly illegal—telemarketing calls and texts damages our trust in our phones and makes it more difficult for important messages from health care providers and other legitimate callers to get through.

In addition, NCLC filed 15 sets of comments and letters with the FCC this year, urging strong regulations to protect consumers from scam calls and texts.

In December, NCLC led advocates in applauding the FCC for voting to clarify its rules on telemarketing calls by unequivocally prohibiting the abuse of consumer consent by lead generators.

Student Loans

NCLC kicked off 2023 by joining borrower advocates and legal aid organizations in submitting an amicus brief to the U.S. Supreme Court arguing that COVID-19 made student debt relief a necessity for low-income borrowers. NCLC kept consumer advocates apprised of developments in the case, including via a web article on NCLC.org explaining the two cases before the Supreme Court and how the outcome of these cases would affect the millions of borrowers eligible for relief.

Following the Supreme Court’s 6-3 decision to block President Biden’s student debt relief program, advocates produced a post on NCLC.org focused on protecting student borrowers and a Digital Library article focused on borrower rights after the ruling.

NCLC advocates also applauded the Department of Education’s announcement that it would pursue debt relief for borrowers using alternative authority. NCLC submitted extensive comments in response to the Department’s request for comment on its plan to develop new rules through which to provide debt relief. NCLC staff attorney Kyra Taylor was selected to serve on the Department’s rulemaking committee. That rulemaking should wrap up in 2024 and has the potential to provide significant relief to low-income borrowers who have struggled for years or even decades with unaffordable student debt and snowballing interest.

Advocates also applauded action by the Department of Education to begin discharging $39 billion in Federal student loans held by borrowers who had been in repayment for twenty years or more already–helping more than 804,000 borrowers get out from under crushing student debt. But we warned that more must be done.

In June, NCLC’s Student Loan Borrower Assistance project launched a newly updated, consumer-facing website with resources and advice for borrowers and for media to share with borrowers, as well as a portal through which borrowers can share their stories with NCLC to support policy advocacy. Throughout the second half of the year, NCLC published blog posts explaining what borrowers need to know about the return to repayment and key relief opportunities, including the U.S. Department of Education’s time-limited Fresh Start initiative to help borrowers get out of default, the repayment count adjustment which will finally give debt relief to hundreds of thousands of borrower, and the new SAVE repayment plan. NCLC also conducted numerous trainings on these programs and ran a half-day intensive student loan training program at the Consumer Rights Litigation Conference.

NCLC also advocated for rules to help prevent low-value schools from preying on students for their federal student aid dollars. NCLC submitted public comments on the proposed gainful employment rule and other proposals to enhance transparency and accountability in higher education. NCLC also submitted comments in response to the Department’s announcement of its intent to form a negotiated rulemaking committee to address program participation in federal student aid programs, and NCLC advocate Robyn Smith was nominated to represent legal aid organizations that serve low-income borrowers on the negotiated rulemaking committee.

Advocates worked to make student loan relief programs more accessible to borrowers by advocating for improvements to the application processes, including by submitting comments in response to the U.S. Department of Education’s request for feedback on the proposed application form for the Total and Permanent Disability (TPD) Program and comments in response to the U.S. Department of Education’s proposed income-driven repayment (IDR) plan request form.

NCLC also joined a coalition letter in strong opposition to efforts to use the Congressional Review Act (CRA) to overturn the Biden-Harris Administration’s new rule implementing the Saving on a Valuable Education (SAVE) Plan.

Finally, in the issue brief Delivering Distress to Borrowers in Default, advocates explained who is in student loan default and why, and the devastating consequences of default. The issue brief identified legal authority that empowers the Secretary of Education to compromise student loan debts and so end collection from defaulted borrowers where such efforts would be futile or unreasonable.

Support NCLC

Please support NCLC's work to advance consumer rights and economic justice with a tax-deductible contribution today!

Donate