WITH: COLIN WEIDIG, CAMILLE DESIERTO, MARYANN FLANAGAN, RACHEL SCOTT

There are roughly 480,000 reverse mortgages currently outstanding in the United States. This number is expected to grow as baby boomers age. The program was designed to allow older homeowners to borrow against their home equity without the risk of displacement, but reverse mortgages end in foreclosure much more often than they should. Reverse mortgage borrowers who fall behind on property charges face significant hurdles to obtaining a narrow set of home retention options. Heirs struggle to access information necessary to satisfy the reverse mortgage without the need for foreclosure. Spouses who are not listed on loan documents, often termed “non-borrowing spouses,” can generally remain in the home if they keep paying the property taxes, but are not eligible for loss mitigation. Servicers too often foreclose based on supposed non-occupancy when the borrower is still occupying the home. Across all of these situations, poor servicing communication and insufficient access to housing counseling exacerbate the problems.

Resolving these problems is particularly important because of the effect of preventable reverse mortgage foreclosures on the racial wealth and homeownership gap. The crisis of preventable reverse mortgage foreclosures does not impact all communities equally. Historically, people of color have been more likely to take out reverse mortgages, due to the legacy of discrimination and policies that limited their wealth-building opportunities, and they are also more likely to end up in reverse mortgage foreclosure. The heirs of reverse mortgage borrowers of color may lose significant home equity if they are not able to sell or refinance the home to satisfy the loan. When it comes to addressing the racial wealth gap and racial homeownership gap, reducing the number of preventable reverse mortgage foreclosures is an important and necessary step.

The FHA reverse mortgage program has not lived up to its full potential. Based on the information uncovered in this report, we call on FHA and the Consumer Financial Protection Bureau (CFPB) to act quickly to prevent any additional home losses for this vulnerable population.

Top Four Recommendations for FHA

- Allow flexibility with property charge loss mitigation policies

- Rescind the due and payable status when loss mitigation is approved

- Allow loans to be assigned to FHA while in an active loss mitigation plan

- Require a loss mitigation review

Top Four Recommendations for the CFPB

- Include reverse mortgages in the RESPA mortgage servicing rules

- Work with FHA on effective reverse mortgage communications

- Prioritize reverse mortgage servicer supervision and enforcement

- Require prompt payoff statements

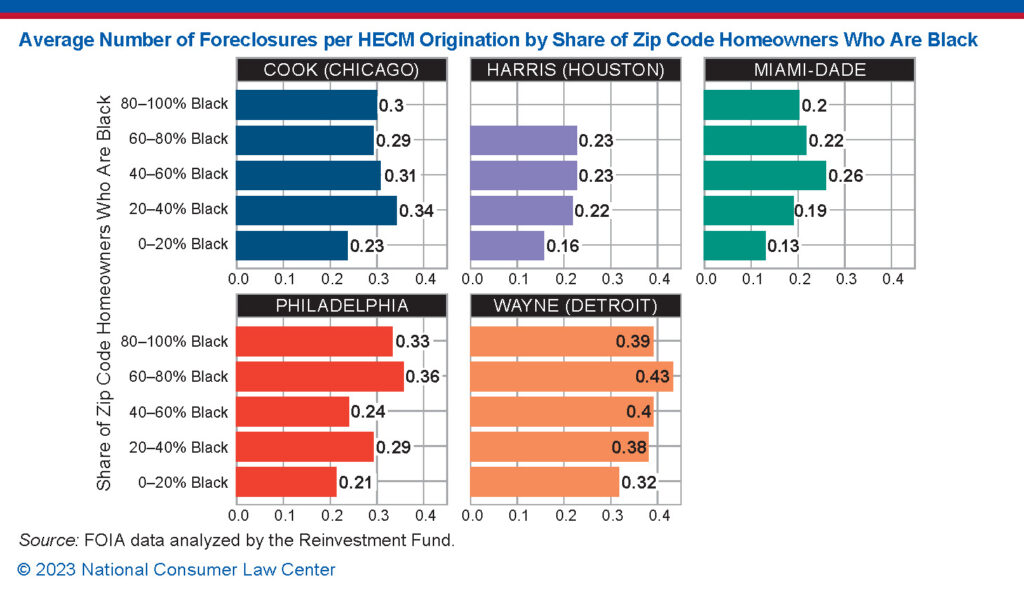

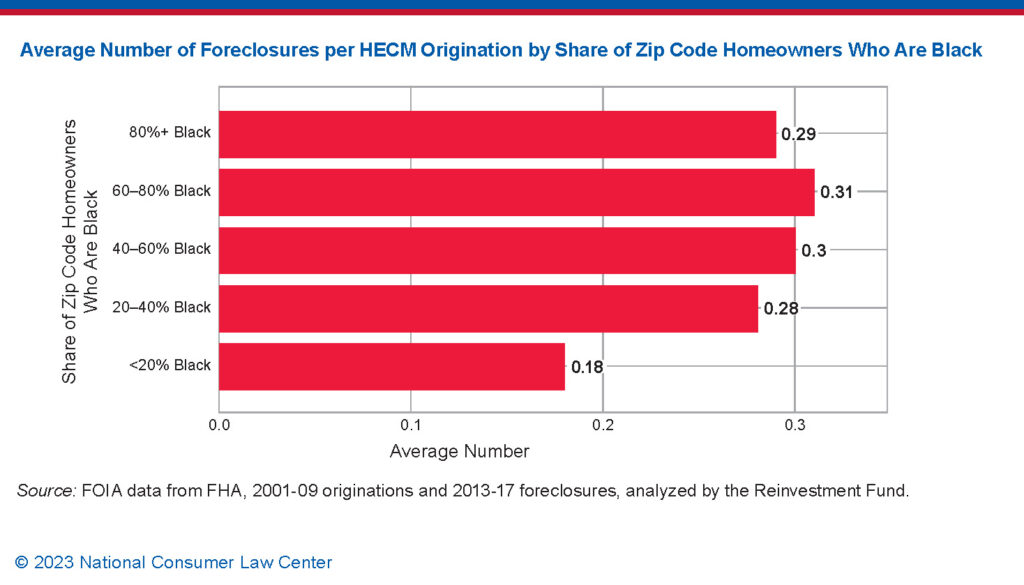

Reverse mortgages, also known as Home Equity Conversion Mortgages (HECMs), are disproportionately concentrated in communities of color. But reverse mortgage foreclosures are even more concentrated. These charts show the ratios of reverse mortgage foreclosures to originations by percent Black for all five metro areas examined in the report.

See all resources related to: Homeownership & Foreclosure