This is an outdated report. For the most current version click here.

Caps on interest rates and loan fees are the primary vehicle by which states protect consumers from predatory lending. Forty-five states and the District of Columbia (DC) currently cap interest rates and loan fees for at least some consumer installment loans, depending on the size of the loan. However, the caps vary greatly from state to state, and a few states do not cap interest rates at all.

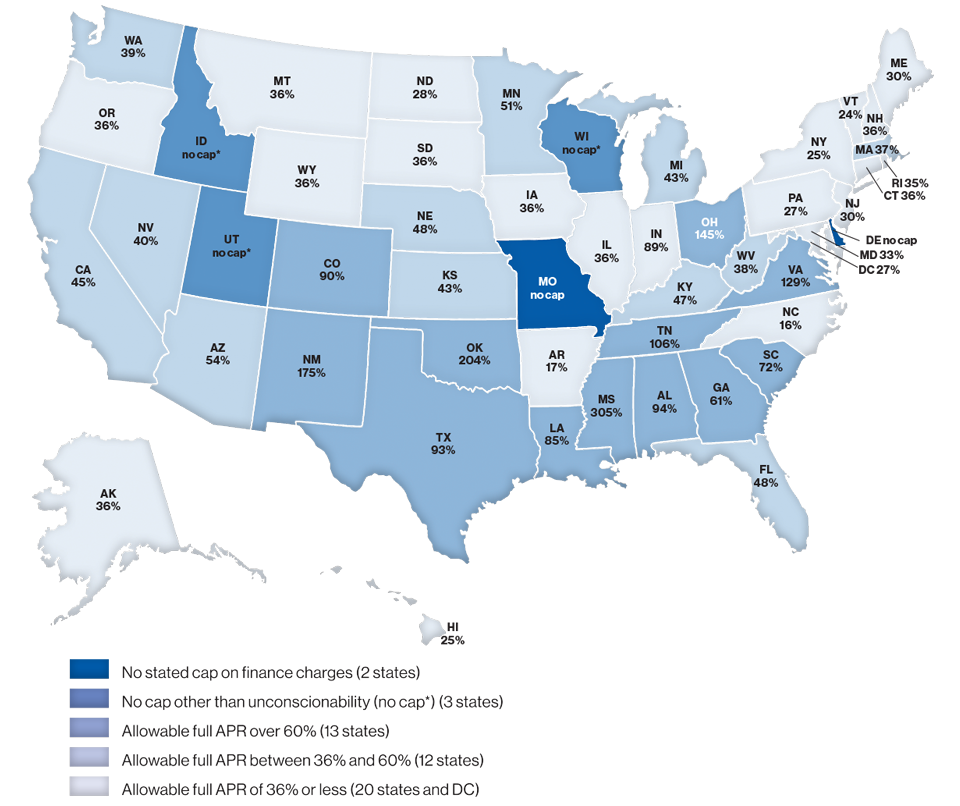

For a $500, six-month installment loan, 45 states and DC cap rates, at a median of 38.5%.

- 20 states and the District of Columbia cap the annual percentage rate (APR) at 36% or less.

- 12 states cap the APR between 36% and 60%.

- 13 states cap the APR above 60%.

- Three states—Idaho, Utah, and Wisconsin—require only that the loan not be “unconscionable” (a legal principle that bans terms that shock the conscience).

- Two states–Delaware and Missouri–impose no cap at all.

Map 1: APRs Allowed for Six-Month $500 Installment Loan

These maps show the maximum APRs allowed by the states for closed-end installment loans (loans in which the amount borrowed and the repayment period are set at the outset) by non-bank lenders.

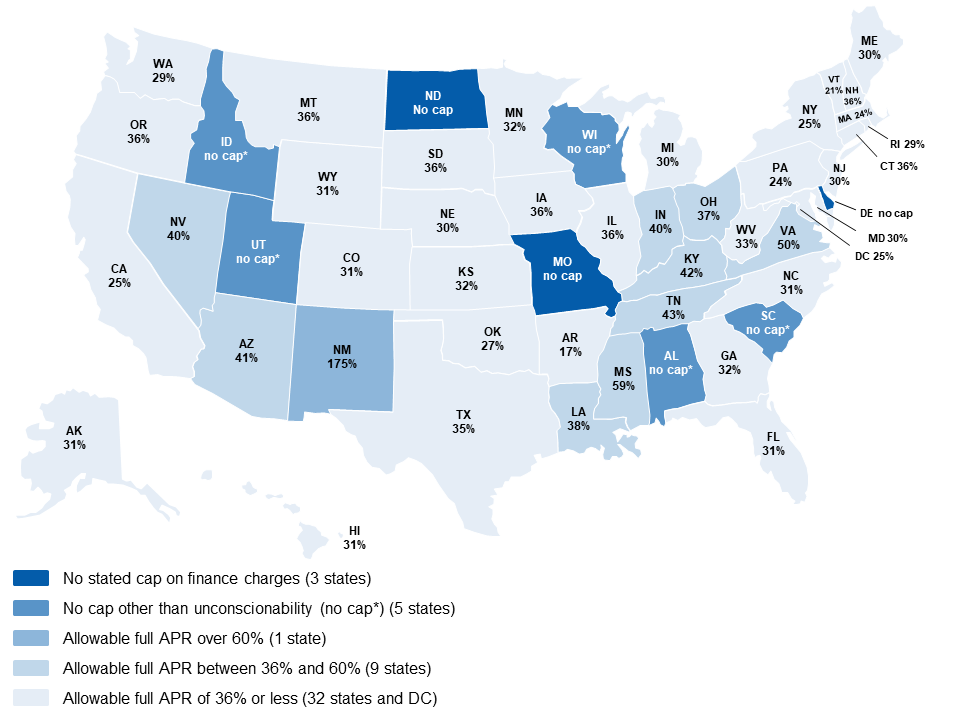

For a $2,000, two-year installment loan, 42 states and DC cap rates, at a median of 32% APR.

- 32 states and the District of Columbia cap the APR at 36% or less.

- 9 states cap the APR between 36% and 60%.

- New Mexico caps the APR at 175%.

- Five states—Alabama, Idaho, South Carolina, Utah, and Wisconsin—require only that the loan not be “unconscionable.”

- Three states–Delaware, Missouri, and North Dakota–impose no cap at all.

Map 2: APRs Allowed for Two-Year $2,000 Installment Loan

Why States Should Cap Interest Rates and Fees

Caps on interest rates and loan fees are the primary vehicle by which states protect consumers from predatory lending. In the absence of rate caps, exploitive lenders move into a state, overwhelming the responsible lenders and pushing abusive loan products that trap low-income consumers in never-ending debt.

Interest rate caps are more than numbers: they are reflections of society’s collective judgment about moral and ethical behavior. Interest rate caps embody fundamental values.1 Interest rate caps also reflect an assessment about the upper limits of sustainable lending that does not undermine individual or societal economic stability.

In addition to limiting the cost of the loan for the borrower, limits on finance charges encourage lenders to ensure that the borrower has the ability to repay the loan. Excessive interest rates enable lenders to profit from loans even if many borrowers eventually default.2 Knowing that it will be made whole even if the borrower defaults, or that it can recoup defaults from exorbitant rates on others, the lender has little incentive to ensure that each borrower can actually afford to repay the loan in full on its terms.

High-cost lending also has a disproportionate impact on communities of color.3 Payday lenders have long targeted these communities.4 High-cost loans do not promote financial inclusion; they drive borrowers out of the banking system and exacerbate existing disparities.5

The APR is an Essential Standard for Measuring and Comparing the Cost of a Loan

The rates listed above are the annual percentage rates (APRs) as calculated under the Truth in Lending Act (TILA) for installment loans and include both periodic interest and fees. The APR is a critical way to measure and compare the cost of a loan, because it takes both interest and fees, and the length of the repayment period, into account. It provides an apples-to-apples comparison of the cost of two different loans, even if they have different rate and fee structures or are used to borrow different amounts for different periods of time.

The Military Lending Act (MLA), which places a 36% APR cap on loans to members of the military and their families, requires the APR to take into account not just interest and fees but also credit insurance charges and other add-on charges. The MLA is also far more accurate than TILA as a disclosure of the cost of open-end credit such as credit cards. Because of this, the MLA APR is the gold standard, both for purposes of cost comparison and for purposes of legal rate limits. However, because of the difficulty of identifying the cost of credit insurance and other add-ons allowed, in the abstract, by the various state laws (as opposed to calculating the MLA APR for a given loan), we have used the TILA APR rather than the MLA APR in the rates displayed above.

For detail about how we calculated the APRs, see Appendix D of Predatory Installment Lending in 2017: States Battle to Restrain High-Cost Loans, Aug. 2017.

Significant Changes in the States from 2020 to the Present

Five states have made significant changes affecting their APR caps since the beginning of 2020:

Illinois: On March 23, 2021, Illinois Governor J.B. Pritzker signed S.B. 1792, which imposes a 36% APR cap, calculated using the MLA methodology, on all non-bank loans made in the state. This change is a great improvement for Illinois residents. Formerly, a non-bank lender could charge an APR as high as 99% for a $500 six-month installment loan, and as high as 80% for a $2,000 two-year loan.

Indiana enacted a law, S.B. 395, that increases the already excessive fees that lenders can charge and distorts the interest rate. The result is that non-bank lenders in the state can now charge an APR of 89% for a $500 six-month loan, increased from 71%. For a $2,000 two-year loan the increased fee pushes the APR cap up to 40% from 39%.

Minnesota: The maximum APR for a $2,000 two-year loan in Minnesota increased from 31% to 32% due to adjustments for inflation that its lending laws require every two years.

Virginia overhauled its non-bank lending laws in 2020 by enacting H.B. 789. The law closes loopholes that high-cost lenders were using to evade the state’s rate caps through open-end loans, but the law also authorizes much higher APRs for installment loans: 129% instead of 36% for a $500 six-month loan and 50% instead of 36% for a $2,000 two-year loan.

Tennessee made its already-bad lending laws worse in early 2021 by passing S.B. 344. Effective July 1, 2021, the bill increases the junk fees that non-bank lenders can charge for small loans. Under the new law, a $500 six-month loan can have an APR as high as 121% (up from 94%), and a $2,000 two-year loan can have a 43% APR (up from 42%).

Major changes in the states from 2017 to 2019 are summarized in the table below and described in more detail in NCLC’s February 2020 report on state APR caps.

Table: Significant State Changes from 2017 to 2019

Recommendations: A 36% APR Cap

To protect consumers from high-cost lending, states should:

- Cap APRs at 36% for smaller loans, such as those of $1,000 or less, with lower rates for larger loans.

- Prohibit loan fees or strictly limit them in order to prevent fees from being used to undermine the interest rate cap and acting as an incentive for loan flipping.

- Prevent loopholes for open-end credit. Rate caps on installment loans will be ineffective if lenders can evade them through open-end lines of credit with low interest rates but high fees.

- Ban the sale of credit insurance and other add-on products, which primarily benefit the lender and increase the cost of credit, or require their cost to be included in the APR cap, as the Military Lending Act does for loans made to servicemembers.

- Examine consumer lending bills carefully. Predatory lenders often propose bills that obscure the true interest rate, for example, by presenting it as 24% per year plus 7/10ths of a percent per day instead of 279%. Or the bill may list the per-month rate rather than the annual rate. Get a calculation of the full APR, including all interest, all fees, and all other charges, and reject the bill if it is over 36%.

The 36% rate cap is a widely accepted measure of the top acceptable rate and has been broadly supported by both lenders and the general public.6 But for loans in the thousands of dollars, 36% is too high, and a tiered structure that lowers rates as loans get bigger is appropriate. For example, for loans up to $10,000, Alaska allows 36% on the balance up to $850, and 24% on the remainder, with no additional fees.7

In addition, states should make sure that their loan laws address other potential abuses. States should:

- Require lenders to evaluate the borrower’s ability to repay any credit that is extended.

- Prohibit mechanisms, such as security interests in household goods and post-dated checks, that coerce repayment of unaffordable loans.

- Require proportionate rebates of all up-front loan charges when loans are refinanced or paid off early.

- Limit balloon payments, interest-only payments, and excessively long loan terms. An outer limit of 24 months for a loan of $1,000 or less and twelve months for a loan of $500 or less might be appropriate, with shorter terms for high-rate loans.

- Employ robust licensing and reporting requirements, including default and late payment rates, for lenders.

- Include strong enforcement mechanisms, including making unlicensed or unlawful loans void and uncollectable and providing a private right of action with attorneys’ fees.

- Tighten up other lending laws, including credit services organization laws, to prevent evasions.

See NCLC’s 2015 report on high-cost small loans for more details on each of these recommendations.

In the absence of rate limits at the federal level, state interest and fee caps are the primary bulwark against predatory lending. By following these guidelines, states can ensure that their laws are effective at protecting consumers.

Authors and Acknowledgments

Co-authors: Carolyn Carter, deputy director, National Consumer Law Center; Lauren Saunders, associate director, National Consumer Law Center; Margot Saunders, senior counsel, National Consumer Law Center. The authors thank NCLC colleagues Maggie Westberg, Jan Kruse, Moussou N’Diaye and Stephen Rouzer for assistance. The authors also thank the Annie E. Casey Foundation, whose support of our work made this report possible. The findings and conclusions presented in this report are the authors’ and do not necessarily reflect the views of the funder.

Endnotes

1 See National Consumer Law Center, CONSUMER CREDIT REGULATION § 1.4 (3d ed. 2020) (tracing the origin of the general usury laws on the books in many states today to England’s laws before American independence).

2 National Consumer Law Center, Misaligned Incentives: Why High-Rate Installment Lenders Want Borrowers Who Will Default (July 2016).

3 S. Ilan Guedj, Ph.D., Report Reviewing Research on Payday, Vehicle Title, and High-Cost Installment Loans at 9 (May 14, 2019).

4 See, e.g., Brandon Coleman & Delvin Davis, Center for Responsible Lending, Perfect Storm: Payday Lenders Harm Florida Consumers Despite State Law at 7, Chart 2 (March 2016).

5 CFPB, Online Payday Loan Payments at 3-4, 22 (April 2016).

6 See Lauren Saunders, National Consumer Law Center, Why 36%? The History, Use, and Purpose of the 36% Interest Rate Cap, April 2013.

7 Alaska Stat. § 06.20.230.

Related Resources

- Press Release

- NCLC’s Payday & Installment Loans page

- Report: Why 36%? The History, Use, and Purpose of the 36% Interest Rate Cap, April 2013

- State Rate Caps for $500 and $2,000 Loans, March 2021

- Report: Predatory Installment Lending in the States: 2020, February 2020

- Report: A Larger and Longer Debt Trap?: Analysis of States’ APR Caps for a $10,000 Five-Year Installment Loan, October 2018

- Report: Predatory Installment Lending in 2017: States Battle to Restrain High-Cost Loans, Aug. 2017

- Report: Misaligned Incentives: Why High-Rate Installment Lenders Want Borrowers Who Will Default, July 2016

- Report: Installment Loans: Will States Protect Borrowers from a New Wave of Predatory Lending?, July 2015

Publications

- Attorneys/Advocates: Consumer Credit Regulation (see chapters 9 & 10)

- Consumers: Surviving Debt

See all resources related to: High-Cost Credit