The largest banks continue to take billions of dollars a year in overdraft fees from families facing an affordability crisis. Some banks in particular stand out for their high or rising fee revenues, according to the latest call report data. In 2025, banks and credit unions extracted over $12 billion in overdraft and nonsufficient funds (NSF) fees from struggling families.

About a quarter of people live in households that pay overdraft fees each year. The fees fall disproportionately on Black and other nonwhite households, those with lower incomes, and those with limited education.

A 2024 rule from the Consumer Financial Protection Bureau (CFPB) was expected to save households $5 billion a year or $225 a year for families that pay overdraft fees. But the CFPB overdraft fee rule was reversed by Congress in 2025. In the lead up to the rule, many banks had made voluntary changes to reduce or eliminate fees as a result of regulatory pressure. With pressure from the federal government off, progress has stalled, and some banks have begun increasing their fees. Now, states must step in.

Overdraft Fees Hall of Shame

Overall, overdraft revenues at the top 20 banks were up 6.2% in 2025 over 2023, when the CFPB last published figures, and the increase was far higher at some banks. Several banks stand out:

- JP Morgan Chase and Wells Fargo continue to lead the pack, taking about $1 billion each a year in overdraft fees. Chase collected $1.1 billion, slightly up from 2023, and Wells Fargo took $924 million, slightly down from 2023. PNC Bank, which is

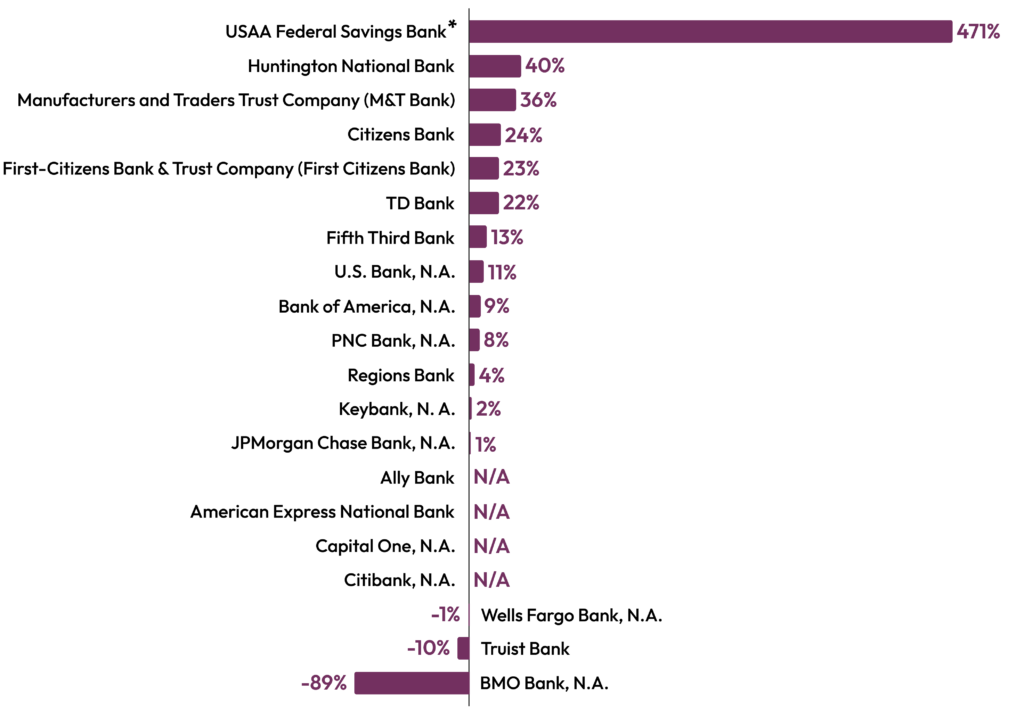

significantly smaller, was third in overall overdraft revenues at $279 million, up a significant 8% over 2023. - USAA Federal Savings Bank, which caters to the military community, has dramatically increased its overdraft fee revenue since 2023, by a larger percentage than any other bank, primarily by introducing overdraft fees in late 2023. There were also large increases at Huntington Bank (40%), M&T Bank (36%), Citizens Bank (24%), First Citizens (23%), and TD Bank (22%).

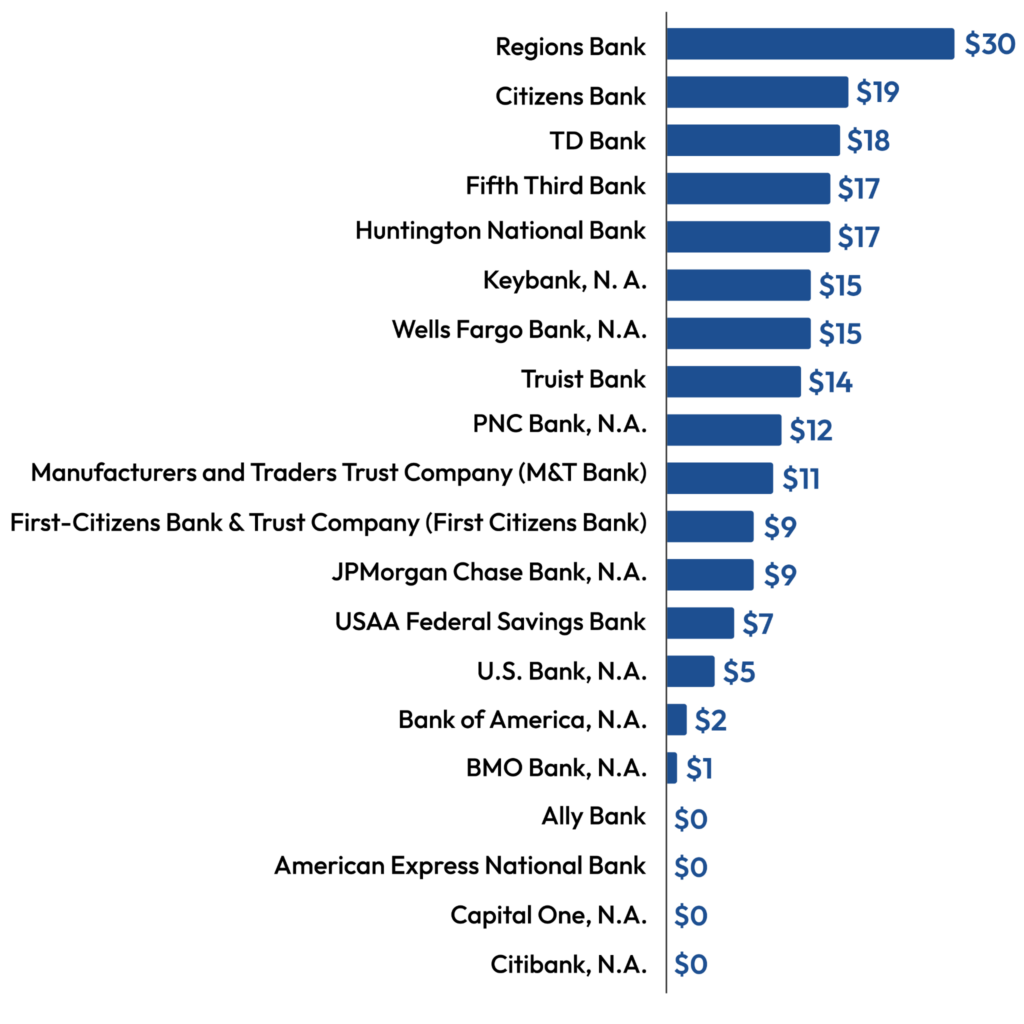

- On a per account basis, Regions Bank had the most overdraft fee revenues among large banks at $30 a year on average (and more of course for some families). Citizens Bank ($19), TD Bank ($18), Fifth Third Bank ($17), and Huntington National Bank ($17) also had high fees per account compared to other banks, as did Wells Fargo ($15).

- While not among the 20 largest banks, three other banks previously highlighted by the CFPB for high overdraft fee revenues also collected especially large amounts of overdraft fees per account in 2025: Woodforest Bank, with a whopping $94 per account per year; First Convenience Bank at $68 in overdraft and NSF fees per account; and Arvest Bank, at $45 a year in overdraft fees. Overdraft revenues are no longer available for credit unions after the National Credit Union stopped requiring reporting of that data, but in 2024 Navy Federal Credit Union had $28 in overdraft fees per account, higher than all but one of the top 20 banks.

Collectively, the top 20 consumer banks earned $4 billion in overdraft fee revenue in 2025. In 2024, the total for all banks and credit unions was estimated to be $12.1 billion. Assuming the same increase from 2024 to 2025 across the industry as for the top 20 banks (it could be more or less), people paid an estimated $12.4 billion in overdraft and NSF fees in 2025.

Positive Developments

On the plus side:

- Capital One, Citibank, American Express, and Ally Bank charge no overdraft fees.

- None of the top 20 banks charges NSF fees.

- BMO Bank’s overdraft revenue dropped significantly from $27 million in 2023 to $2 million in 2025 following a reduction in fees from $36 to $15. However, BMO backtracked in 2026, raising fees to $20 and reducing the overdraft cushion that does not trigger a fee from $50 to $20.

- Truist Bank also had a 10% drop in overdraft fees over 2023.

Going Backwards Under the Trump Administration

Overdraft fees were slated to go down dramatically after the CFPB issued a rule in 2024 reducing most overdraft fees to $5, saving the average household that pays overdraft fees $225 per year. But Congress overturned that rule in 2025, and it never went into effect.

In addition, under the Trump Administration, the CFPB and banking agencies took several other actions that relieved the pressure on banks and credit unions to address abusive overdraft and NSF fee practices. The CFPB rescinded a consent order on Navy Federal Credit Union that had been imposed due to Navy Fed’s practice of charging surprise overdraft fees when people had money in their account at the time of the transaction. The CFPB also rescinded guidances warning banks about surprise overdraft fees and about charging fees on debit cards without proof that the person consented to overdraft coverage. The FDIC dropped a rule that prohibited banks under its supervision from charging more than one NSF fee for the same bounced item. The National Credit Union Administration stopped collecting data on overdraft fee revenue.

States Need to Act

States do not have the same full power over banks that the federal government has due to preemption provisions in banking laws. However, they still have the ability to take action to limit overdraft and NSF fees, especially by banks and credit unions chartered in their states, and to keep the spotlight on unfair practices. A new NCLC report describes the actions states can take. In particular, the report urges states to:

- Limit overdraft fees to $5

- Prohibit NSF fees

- Allow banks and credit unions to collect no more than six overdraft fees per year or fees totaling no more than $200 a year

The report also outlines other actions states can take to address abusive practices that cause people to incur excess fees and to spotlight the banks and credit unions that collect an inordinate amount of fees from struggling consumers.

Overdraft Fee Revenues Among the 20 Largest Consumer Banks

The following charts (see below) list the overdraft fee revenues for the 20 largest consumer banks, excluding those that are primarily investment banks or that otherwise do not hold a significant number of checking accounts for low-wealth individuals. The data are taken from call reports submitted to the Federal Financial Institutions Examination Council (FFIEC). The relevant line item on the call reports includes both overdraft and NSF fees, but none of the top 20 banks charges NSF fees, so for them the revenue is entirely overdraft fees.

2025 Overdraft Fee Revenue, Top 20 Consumer Banks

2025 Overdraft Fee Revenue Per Account, Top 20 Consumer Banks

Change in Overdraft Revenue, 2023 to 2025, Top 20 Consumer Banks

See all resources related to: Banking, Payments & Remittances