OVERVIEW

In a responsible loan market, the lenders’ profits are closely aligned to the successful repayment of the credit. Yet high-rate installment lending can lead to asymmetrical incentives:

As long as the borrower pays long enough before defaulting, a high-rate installment loan will be profitable. If the borrower makes even half the payments on a longer term high-rate installment loan, the lender may receive sufficient cash flow to recover the amount loaned and another 50% or more, likely more than enough to turn a profit. While the lender may have a successful experience, default causes a cascade of devastating consequences that are likely to plague the consumer for a lifetime.

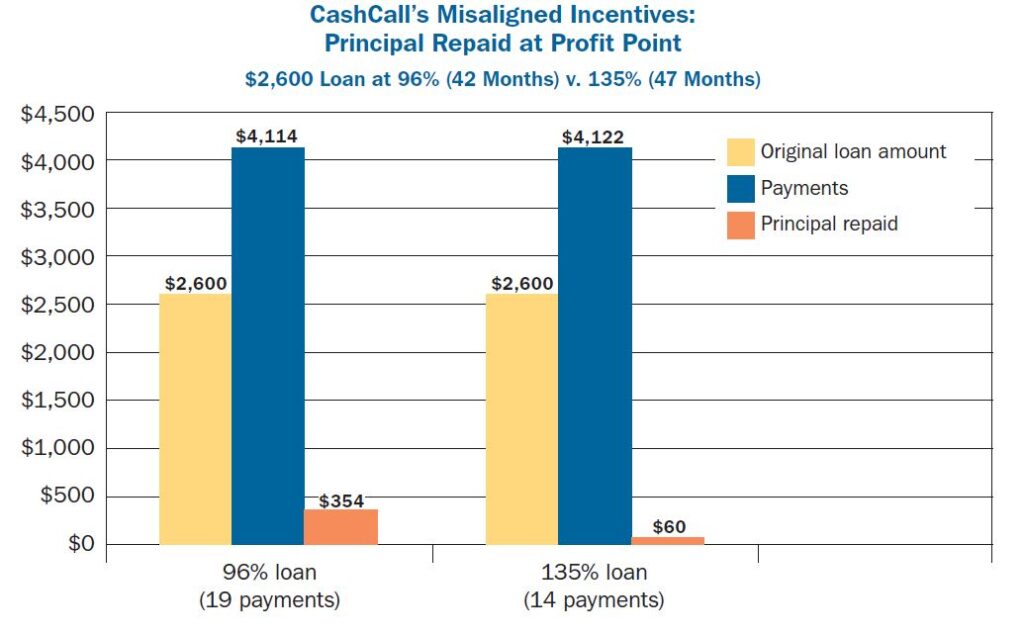

A borrower who defaults later can be a more profitable customer than one who prepays the loan in full too early. Tighter underwriting can lead to borrowers who are able to repay early, generating less revenue than a consumer who struggles for months or years to make payments and then ultimately defaults.

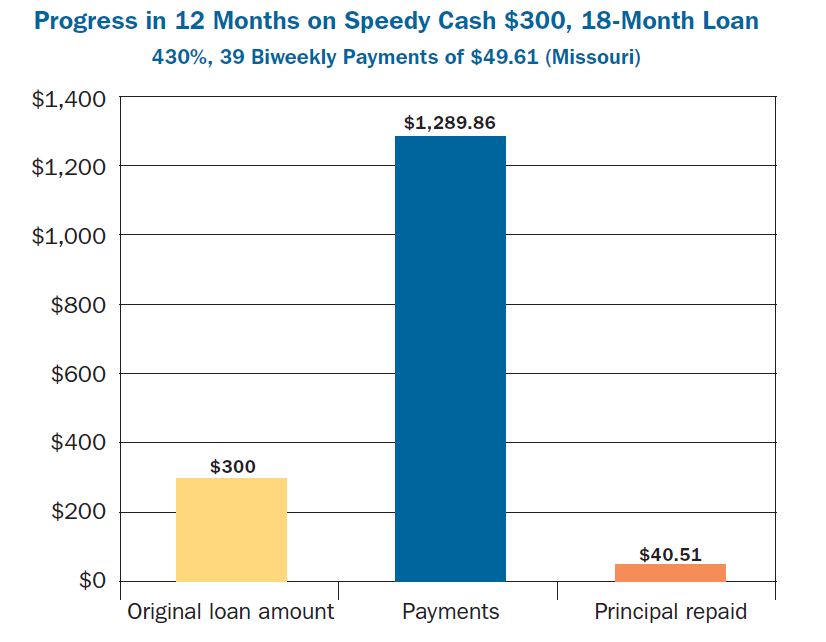

Skewed incentives are most pronounced in larger, longer-term loans. But a misalignment of lender and borrower success can also occur with smaller or shorter loans, especially those with high rates, disproportionately long terms or repeat refinancing. A small loan with a long term functions like a series of short-term payday loans with payments that do not reduce the amount owed for many months. Borrowers may not be able to keep up even with relatively small payments, but the lender may still make a profit. Even on shorter 6-month loans, triple-digit lenders can often recover the amount loaned if the borrower makes only half of the payments.

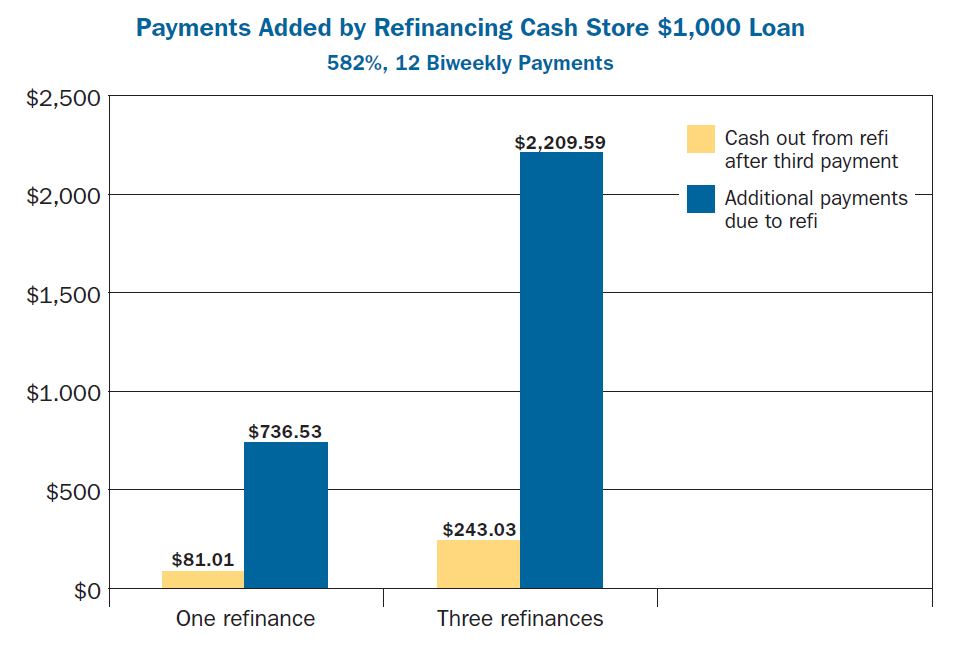

Refinancing can increase the gap between lender and borrower success. A refinancing that gives the consumer barely enough cash to cover one payment can add three, four, or even six payments to the time in debt, increasing the possibility that the consumer will default before reaching the end.

High default rates are common among high-rate installment lenders. Data collected by California reveal default rates from 20% to 40% or even higher among high-rate installment lenders, compared to default rates of 2% to 9% for companies that make lower interest rate loans to California consumers with subprime credit scores. The charge-off rates for high-rate lenders in California are 1,000% to 2,000% higher than national credit card charge-off rates.

Defaults are just the tip of the iceberg of borrower pain caused by unaffordable lending. When delinquencies are added to defaults, the “struggling index” for some lenders in California rises to 30% or even 80% or higher. Even loans that do not default can be a destructive experience for struggling borrowers.

KEY RECOMMENDATIONS

Legislators, regulators and enforcement authorities should take action to change these misaligned incentives and narrow the gap between lender and borrower success:

- The easiest and most effective way to align the interests of lenders and borrowers and to minimize defaults is to cap interest rates (including fees) at 36% (lower for larger loans, such as those over $1,000). At lower interest rates, the lender and borrower together will benefit from a successful loan and feel pain from an unsuccessful one. Rate caps should apply to all consumer and small business loans regardless of size.

- Lenders should be prohibited from making loans that borrowers cannot afford to repay on the loan’s original terms while meeting other expenses without reborrowing.

- Regulators should monitor and collect data on default rates and other indicators of unaffordable lending. Data should be collected on default rates on a per-consumer and loan-cohort basis, as well as on rates of refinancing, late fees, delinquencies, and bounced or missed payments.

- Default rates above 10% (or lower for auto title, payroll deduction, and other loans with strongly coercive repayment mechanisms) should face scrutiny. The lender’s interest rates, as well as the leniency or aggressiveness of its collection practices, should factor into what level of defaults reflects unfair, deceptive or abusive practices.

- Lenders with high default rates should be found to be in violation of rules prohibiting unfair, deceptive, or abusive practices.

See all resources related to: High-Cost Credit