Everything that is wrong with a high-cost loan is only made worse when the loan is larger

and longer. A larger, longer high-cost loan can be a deeper, longer debt trap than a payday

loan.

Interest rate caps are therefore just as important, and indeed more so, for larger, longer

loans as for small dollar loans. And, since the borrower will pay the interest on a larger

amount over a longer period of time, the rate cap should be substantially lower than the cap

for a smaller, short-term loan. An interest rate that is reasonable for a small loan can lead to

explosive and unaffordable interest on a larger loan. Increasing the interest rate from 25% to 36% adds over $4,000 to the cost of a $10,000, 5-year loan.

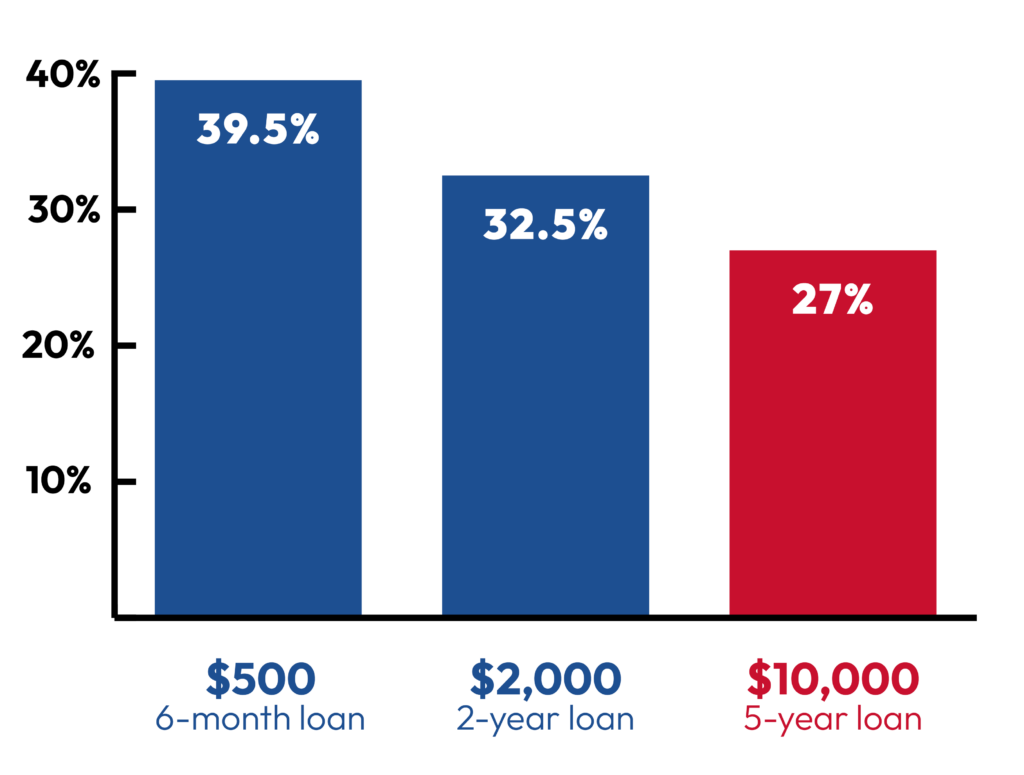

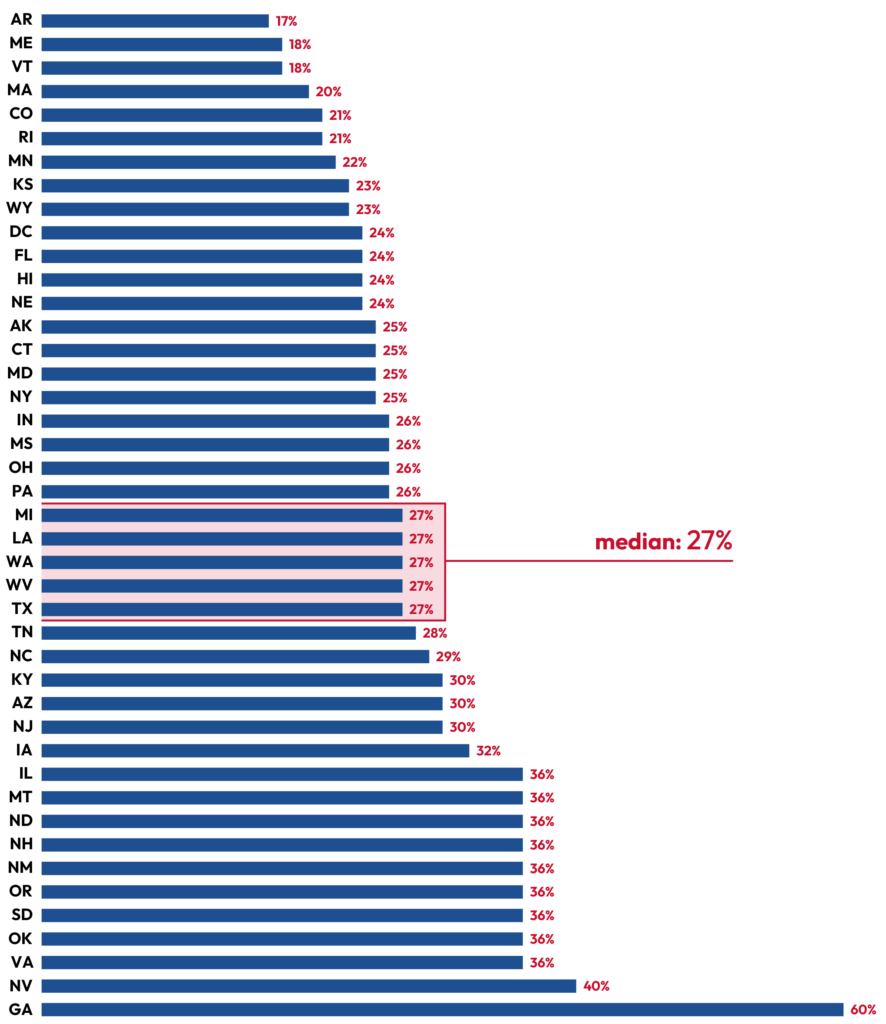

While 36% has become the widely accepted metric for an affordable small dollar loan, most states understandably do not permit that rate for larger loans. The great majority of states cap the interest rate and fees for a five-year $10,000 loan, and in these states the median cap is an Annual Percentage Rate (APR) of 27%. By contrast, the median is 39.5% for a 6-month $500 loan and 32% for a 2-year $2,000 loan. But even 27% is a high rate, especially for larger loans, and 20 states plus the District of Columbia impose lower rate caps on a $10,000 loan.

This report surveys the interest rates and loan fees allowed by all 50 states and the District of Columbia for an unsecured 5-year installment loan of $10,000. It updates our 2018 report, A Larger and Longer Debt Trap? Analysis of States’ APR Caps for a $10,000 Five-Year Installment Loan. The appendix to this report details our methodology. More detail about high-cost installment lending can be found in other reports in this series.

How the States Rate

Forty-two states and the District of Columbia cap the interest rate for a 5-year, unsecured installment loan of $10,000 from a licensed non-bank lender, including all fees that the consumer must pay to get the loan, at a median cap of 27% APR.

See all resources related to: High-Cost Credit