The Consumer Financial Protection Bureau (CFPB) is currently working on a proposed regulation to update its mortgage servicing rule to permanently allow for streamlined loss mitigation reviews. The National Consumer Law Center (NCLC) conducted a nationwide survey in January 2024 to shed light on certain ongoing challenges that create an elevated risk of foreclosure. More than 100 HUD-certified housing counselors and legal services attorneys working in 26 states responded to the survey.

The survey results, highlighted in this report, show that the Bureau, while updating the mortgage servicing rule, should address gaps in the current regulation that leave particularly vulnerable homeowners at risk:

- heirs who inherit a home subject to a mortgage (successors in interest);

- homeowners with long-dormant “zombie” second mortgages, including home equity lines of credit (HELOCs); and

- borrowers with limited English proficiency (LEP).

Older adults, women, and communities of color are disproportionately impacted. Successor in interest challenges disproportionately impact older adults, as most people inheriting the home of a spouse or parent are in their 60s or older. Older adults may also face technological barriers that make it difficult for them to communicate with servicers, particularly in the immediate aftermath of a family member’s death. The harm also falls disproportionately on women, as they are more likely to survive a male spouse and to have been a non-borrower on the home loan due to the wage gap. Moreover, like so many economic justice issues, the burden of these mortgage servicing problems is also hitting the hardest in communities of color due to lower accumulated wealth and a slower full economic recovery after the COVID-19 pandemic. For these communities, successor issues threaten their ability to build and transfer generational wealth.

Survey Findings

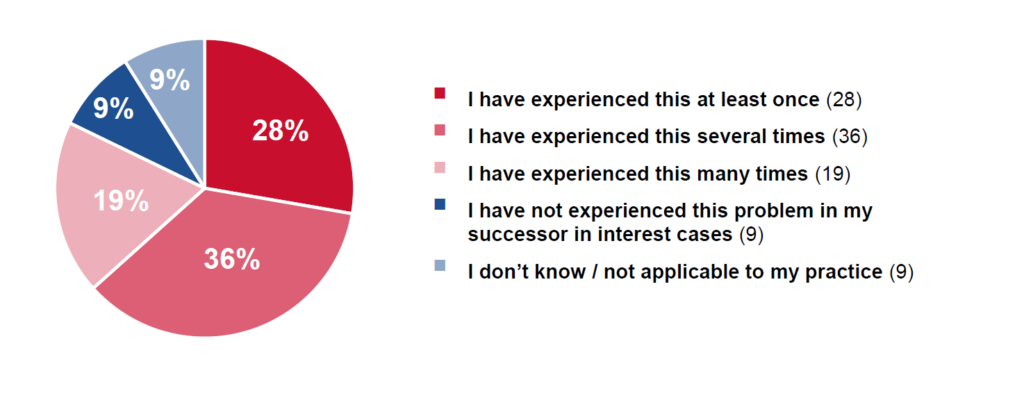

Struggling to get confirmed. More than 80% of respondents reported that they had worked with clients who, despite sending the documentation reasonably necessary to show their identity and ownership interest, still struggled to get a servicer to confirm their status. Over half of respondents said they had experienced this “several” or “many” times:

Have you been in contact with a successor in interest who is struggling to get the servicer to agree they are a “confirmed” successor despite the fact that they have sent all the documentation that is reasonably necessary to show their identity and ownership interest? (Survey Question 3, 101 Responses)

HELOC zombie second mortgages. Borrowers with home equity lines of credit (HELOCs) have the same problems—and therefore need the same protections—as closed-end mortgage borrowers. This is particularly true once the home equity line has been fully drawn and the borrower is in the repayment period. Almost two thirds of respondents surveyed had seen instances where a zombie second mortgage was a home equity line of credit (HELOC). Roughly 40 percent of respondents had seen this several or many times.

Have you seen instances of zombie second mortgages where the zombie mortgage was a home equity line of credit (HELOC)? (Question 14, 86 Responses)

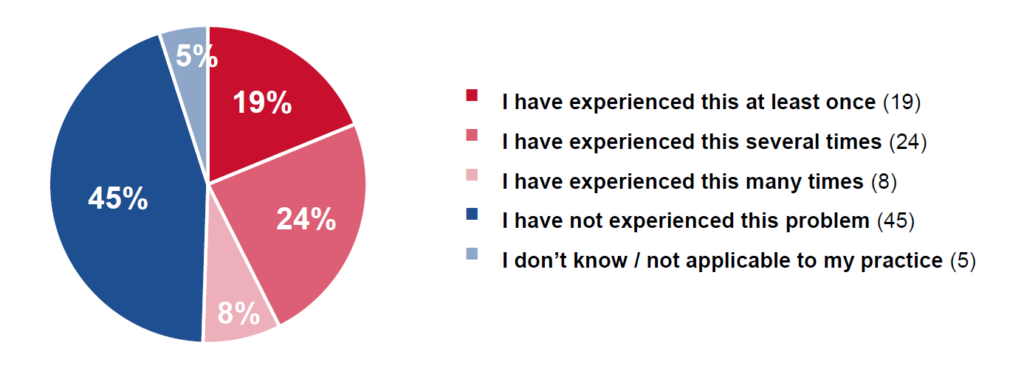

LEP Consumers struggling. Language barriers in the loss mitigation process block consumers with limited English proficiency from accessing measures that could save their home in a timely manner.Over half (51%) of survey respondents indicated that they had been in contact with LEP homeowners who, because all relevant notices were sent in English, struggled to obtain loss mitigation options. Nearly one third of respondents had experienced this with their clients several or many times.

Have you been in contact with a homeowner with limited English proficiency who struggled to obtain loss mitigation options due to the fact that all loss mitigation notices were sent in English? (Question 16, 101 Responses)

Recommendations

We call on the CFPB to take the following steps:

Successors in Interest

- The Bureau should modify the definition of a “confirmed successor” to be any person who has provided reasonable proof of successor status.

- In the alternative, the Bureau could create a private right of action when a servicer fails to provide to the potential successor in interest a description of the documents reasonably required to confirm successor status or fails to confirm a successor within certain reasonable timeframes.

- The Bureau should dedicate resources to supervision and enforcement of the successor rule.

- The CFPB should provide dual tracking protections to successors in interest once they have notified a servicer that they are a potential successor in interest.

- These protections should last until the servicer requests and the successor provides reasonable documentation of successor status. Successors need a reasonable amount of time to prove their status and apply for a loan modification before they face loss of the family home.

- The Bureau should include a definition of “borrower” in Regulation X that would include a signatory to the security instrument even if they did not sign the promissory note. This would make sense for the same reasons it made sense to include successors in interest in the definition of borrower: a person is entitled to information and loss mitigation for the mortgage secured by their home.

Zombie HELOCs

- The CFPB should cover HELOCs in the RESPA servicing rules, especially the rules allowing for Notices of Error, Requests for Information, and loss mitigation protections. The billing dispute rights that apply to open-end credit are not equivalent to the NOE and RFI rights in Regulation X.

- For too many borrowers, Regulation X’s current treatment of HELOCs is a one-way street to foreclosure. The statute contains no HELOC exemption, and we disagreed with the decision to preserve the regulatory HELOC exemption in 2013. Significant shifts in the mortgage lending and servicing markets over the last 10 years have further illuminated the need to give HELOC borrowers these important protections.

Consumers with Limited English Proficiency

- The CFPB should act on its knowledge of the unique challenges that LEP mortgage borrowers face in loss mitigation by requiring that servicers provide the most important loss mitigation notices in-language. These documents should always be provided bilingually in English/Spanish.

- These key loss mitigation notices should also include a tag line disclosure directing consumers to a page on the servicer’s website to obtain the notice in other top languages for which the CFPB has provided a model translation.

- Finally, the CFPB should require that all servicers provide qualified oral interpretation services to consumers in a range of languages, and that these services be provided without unreasonable delay in a range of languages, including languages of lesser dispersion.

Other Resources

- Report: Keeping it in the Family: Legal Strategies to Address the Challenge of Heirs Property and Prevent Home Loss (Jan. 2024)

- Letter: Petition for Reg X Rulemaking on HELOCs, Reverse Mortgages, Language Access, and Manufactured Housing (Aug 2023)

- Comments: NCLC, CRL & NHLP Comment to CFPB on Mortgage Refinances & Forbearances (Nov. 2022)

See all resources related to: Homeownership & Foreclosure